Surging Tax in the Booming Housing Market: What Homebuyers, Sellers, and Realtors Need to Know

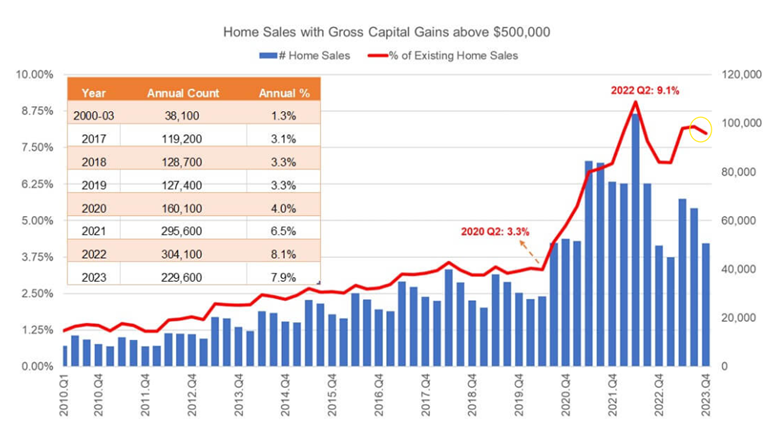

Selling a home in the current market can be incredibly profitable. Yet, this increased profitability brings a significant downside: a growing number of Americans are facing unexpectedly hefty capital-gains taxes. Recent data from CoreLogic, a real-estate data firm, reveals that approximately 8% of home sales in 2023 resulted in gains exceeding the $500,000 tax-free exemption ($250,000 for those filing individually). This is more than double the percentage from 2019. What does this mean for you, the homebuyer, seller, or realtor? Let’s delve deeper.

Understanding the Capital-Gains Tax

Since 1997, individuals and couples selling their primary residence have been able to exclude up to $250,000 and $500,000, respectively, from capital gains taxes. However, this exemption threshold has not changed for over two decades, despite substantial growth in property values, especially during the post-pandemic real estate boom. The static nature of this exemption, combined with soaring home prices, means more homeowners than ever are finding themselves liable for capital-gains taxes once they sell their homes.

The Impact of Inflation

One of the critical issues with the current capital-gains tax exemption is that it isn’t indexed for inflation. This oversight means that as home prices have increased over the years, homeowners are pushed over the exemption limit by normal market appreciation. This kind of increase isn't necessarily reflective of real wealth gain since inflation has greatly devalued the purchasing power of the U.S. dollar.

If you are considering selling your home, it’s crucial to understand the potential tax implications. The windfall from your home sale could lead to a significant tax bill if your profits exceed the exemption limits.

Implementing an Equity Transition Plan

An effective strategy to navigate these challenges is creating an Equity Transition Plan. This strategic approach focuses on optimizing your financial outcomes by minimizing taxes and ensuring your next home purchase aligns with your long-term financial goals. Here’s how it can help:

1. Tax Minimization

By understanding the nuances of the tax implications of your home sale, you can plan your selling timeline and home improvements to maximize your tax-free earnings. For example, investing in home improvements that increase your home's value can help offset some of your gains, thereby keeping you within the exemption limit.

2. Smart Reinvestment

Reinvesting the proceeds from your home sale requires careful planning to avoid financial pitfalls. An Equity Transition Plan helps you assess the best ways to reinvest in real estate or other stable investments. Whether it's purchasing a smaller home, investing in rental properties, or exploring other investment vehicles, the right strategy can safeguard and grow your wealth.

3. Future Planning

Whether you're upsizing, downsizing, or changing locations, your next home purchase should support your lifestyle and financial goals. We can assess how to achieve this within the framework of your overall financial plan. For instance, if you're moving to a new city, understanding the local market dynamics can help you make a more informed decision that aligns with your financial aspirations.

In Conclusion

Selling your home is a major decision with significant financial implications. As real estate markets continue to evolve, it's essential to stay informed and proactive about tax considerations and market trends. Don't navigate this complex process alone. Contact us today to develop your personalized Equity Transition Plan. Together, we'll ensure that you minimize your tax liability and align your home sale with your broader financial objectives, making your success not only more likely but also easier and faster to achieve.

---

This comprehensive guide aims to provide valuable insights for homebuyers, sellers, and realtors. By understanding the surging taxes in the booming housing market and implementing a strategic plan, you can make informed decisions that benefit your financial future.

For personalized advice and to learn more about our services,

contact us today.